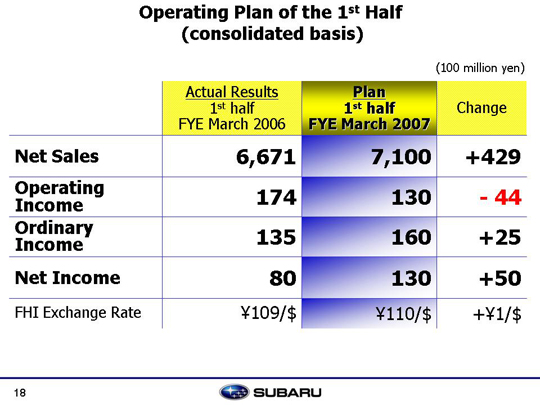

| As for the plan of first half revenue, net sales are expected to increase by 42.9 billion yen as a result of the weak yen effect as well as the new model effect in Japan. Operating income is expected to drop 4.4 billion yen to 13 billion yen due to increasing overhead costs from rising SG&A expenses associated with the introduction of new models in Japan and rising incentive expenses in the U.S. Further details will be described later. Ordinary income is expected to increase by 2.5 billion yen to 16 billion under the condition of no valuation gain or loss from derivatives transactions. Net income is projected at 13 billion yen, because the extraordinary loss caused by termination of the joint development with Saab in the first half of last year will no longer apply. Our non-consolidated sales rate will be 110 yen to the dollar. |